Investing in Portugal’s real estate market offers promising returns, but American and British investors often underestimate the legal complexities, bureaucratic timelines, and hidden costs involved. Without proper preparation, you risk cost overruns exceeding 20% and delays stretching months beyond projections. This guide walks you through the complete investment process, from securing your tax identification to finalizing purchase documentation, ensuring you navigate Portugal’s property market with confidence and realistic expectations.

Table of Contents

- Prerequisites And Legal Requirements For Foreign Investors In Portugal

- Step-By-Step Investment Process In Portugal

- Cost Structure, Financing Options, And Taxation In Portugal

- Common Mistakes And How To Avoid Them

- Expected Investment Results And Market Insights

- Explore Springvale Estates To Optimize Your Portugal Real Estate Investment

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Ownership freedom | Foreign investors face no property ownership restrictions in Portugal regardless of nationality. |

| Timeline reality | Property acquisition typically requires 2.5 to 5 months due to licensing and bureaucratic processes. |

| Cost planning | Total taxes and fees average approximately 11% of the purchase price for property transactions. |

| Budget precision | Detailed Bill of Quantities prevents 20-30% cost overruns during construction phases. |

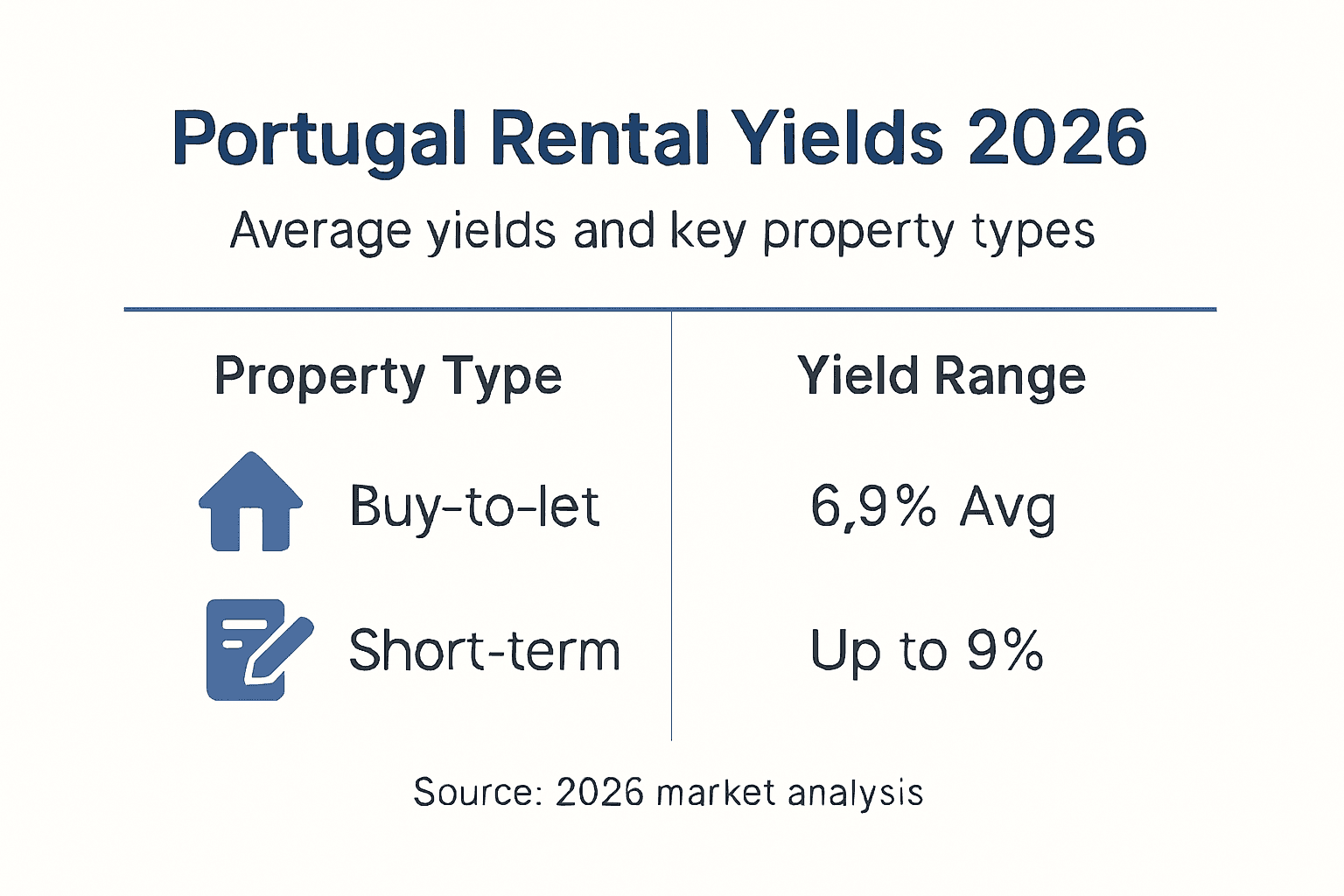

| Return expectations | Buy-to-let properties generate average rental yields around 6.9% across Portuguese markets. |

Prerequisites and legal requirements for foreign investors in Portugal

Portugal welcomes international real estate investment without imposing nationality-based restrictions on property ownership. American and British investors enjoy the same purchasing rights as Portuguese citizens, whether targeting residential apartments in Lisbon or commercial properties in Porto. This open market policy has made Portugal a top destination for foreign capital seeking European real estate exposure.

Before viewing properties, you must obtain a Portuguese Tax Identification Number (NIF). This nine-digit identifier is mandatory for all property transactions, tax filings, and utility account setups. You can apply through Portuguese consulates abroad or authorize a local representative to handle the application in Portugal. Processing typically takes one to two weeks.

Opening a Portuguese bank account is non-negotiable for property purchases. Banks require your NIF, passport, proof of address, and documentation of income sources. Non-resident accounts facilitate mortgage payments, utility bills, and property tax settlements. Expect the account opening process to take two to four weeks, including compliance checks.

Property type selection carries strategic implications beyond purchase price:

- Residential properties offer straightforward rental income and qualify for residency permits

- Commercial properties provide diversified tenant bases but require deeper market knowledge

- New developments may include builder warranties and modern energy efficiency

- Renovation projects demand construction management expertise and permit navigation

The Golden Visa program links certain property investments to residency rights. Qualifying investments currently require minimum thresholds based on property location and type. This pathway appeals to investors seeking European residency alongside portfolio diversification. Program requirements shift periodically, so verify current criteria before committing capital.

Pro Tip: Secure your NIF and bank account before property hunting to demonstrate serious buyer status and accelerate closing timelines when you find the right opportunity.

Step-by-step investment process in Portugal

The Portuguese property investment journey follows a structured sequence with specific documentation requirements at each phase. Understanding this timeline helps you allocate resources appropriately and avoid frustrating delays.

Phase 1: Foundation setup

- Obtain your Portuguese Tax Identification Number through consular services or local representatives

- Open a non-resident bank account with a Portuguese institution

- Engage a qualified Portuguese attorney specializing in real estate transactions

- Define your investment criteria including budget, location preferences, and property type

Phase 2: Market research and property selection

Conduct thorough regional market insights analysis comparing price trends, rental demand, and appreciation potential across target areas. Lisbon and Porto command premium prices with established rental markets, while emerging regions offer higher growth potential with increased risk. Visit shortlisted properties personally to assess condition, neighborhood dynamics, and renovation needs.

Your attorney should review property titles, verify legal ownership, confirm zoning compliance, and identify any liens or encumbrances. This due diligence prevents costly surprises after purchase. Budget at least two weeks for comprehensive legal review.

Phase 3: Financing and offer submission

Non-resident mortgages typically cap at 60-70% loan-to-value ratios, requiring substantial equity contributions. Portuguese banks assess foreign income documentation carefully, demanding translated tax returns, employment contracts, and bank statements covering six to twelve months. Mortgage approval processes consume four to eight weeks.

Submit purchase offers through your attorney, including proposed price, deposit amount, and closing timeline. Successful negotiations result in a promissory contract (contrato promessa) binding both parties. You’ll pay a deposit, usually 10-20% of purchase price, held in escrow pending completion.

Phase 4: Pre-completion requirements

For renovation or construction projects, finalize architectural and engineering plans before engaging contractors. Engaging contractors before design completion inflates budgets and causes project delays. Develop a detailed Bill of Quantities specifying materials, labor, and timeline for each construction phase.

Secure necessary permits from local municipal authorities. Licensing approval timelines vary significantly by municipality and project scope, ranging from one to six months. This bureaucratic phase often extends overall acquisition timelines to 2.5 to 5 months or longer.

Phase 5: Transaction completion

| Step | Timeline | Key actions |

|---|---|---|

| Final deed signing | 1 day | Sign escritura at notary office with all parties present |

| Tax payment | Same day | Pay IMT transfer tax and stamp duty |

| Property registration | 1-2 weeks | Attorney registers ownership with land registry |

| Utility transfers | 1-2 weeks | Transfer water, electricity, and internet to your name |

The notarized deed (escritura) transfers legal ownership. Bring your passport, NIF, and payment proof for all taxes and fees. Your attorney coordinates with the notary to ensure complete documentation. After signing, the property officially becomes yours, though formal registration takes additional time.

Pro Tip: Attend the deed signing personally rather than using power of attorney. Being present ensures you understand all terms and can address any last-minute issues immediately.

Cost structure, financing options, and taxation in Portugal

Budget planning requires accounting for multiple cost layers beyond the property purchase price. Understanding the complete financial picture prevents cash flow surprises and project delays.

Purchase transaction costs

Property transfer tax (IMT) represents the largest transaction expense, calculated on a sliding scale based on property value and type. For properties valued at €550,000, IMT typically reaches approximately 7.5% of purchase price. Add stamp duty at 0.8%, notary fees, registration costs, and legal fees, and total transaction costs approach 11% of purchase price.

| Cost component | Typical amount | Notes |

|---|---|---|

| IMT transfer tax | 6.5-7.5% | Higher for urban properties over €1M |

| Stamp duty | 0.8% | Applied to purchase price |

| Legal fees | 1-2% | Negotiable based on complexity |

| Notary and registration | €500-€1,500 | Fixed administrative costs |

| Property survey | €300-€800 | Recommended for older properties |

Financing considerations for foreign investors

Portuguese banks offer mortgages to non-residents but impose stricter criteria than resident loans. Expect maximum loan-to-value ratios of 60-70%, meaning you must provide 30-40% equity. Interest rates for foreign buyers typically run 0.5-1% higher than resident rates.

Lenders scrutinize income stability and debt-to-income ratios carefully. Provide comprehensive documentation including employment contracts, recent tax returns, proof of existing assets, and credit reports from your home country. Self-employed applicants face additional documentation requirements demonstrating consistent income over multiple years.

Mortgage application processing takes four to eight weeks minimum. Start this process early, ideally before making purchase offers, to understand your financing capacity and strengthen negotiating position.

Ongoing ownership costs

Annual property tax (IMI) ranges from 0.3% to 0.8% of fiscal value, paid in installments. Condominium fees for apartment buildings vary widely based on amenities and services. Budget for property insurance, utilities, and maintenance reserves.

Non-resident property owners pay income tax on rental income at progressive rates up to 48%. Alternatively, you can elect flat-rate taxation at 25% on rental income, often more favorable for higher earners. Consult with Portuguese tax advisors to optimize your structure.

Pro Tip: Work with financial consultation professionals familiar with cross-border taxation to minimize your total tax burden legally through proper entity structuring and deduction maximization.

Common mistakes and how to avoid them

Portuguese real estate investments fail most often due to preventable planning and execution errors. Learning from others’ mistakes saves substantial time, money, and frustration.

Starting construction without detailed specifications

Cost overruns of 20-30% occur when investors begin construction without comprehensive Bills of Quantities. This document specifies exact materials, quantities, labor hours, and costs for every construction element. Without it, contractors provide vague estimates that balloon as work progresses.

Create detailed architectural and engineering plans first. Have quantity surveyors prepare line-item BOQs for contractor bidding. This process takes time upfront but prevents expensive surprises during construction.

Hiring contractors prematurely

Engaging contractors before finalizing designs leads to budget inflation and project delays. Contractors make assumptions about materials and methods when plans remain incomplete, then charge change orders when actual requirements emerge. Design changes mid-construction cost significantly more than adjustments during planning.

Complete architectural plans, obtain necessary permits, and develop full BOQs before soliciting contractor bids. This sequence ensures accurate pricing and minimizes disputes during construction.

Underestimating bureaucratic timelines

Permit approvals, license processing, and administrative procedures in Portugal move slower than in the US or UK. Investors who budget three months for processes requiring six months face financial pressure and rushed decisions. Municipal offices vary dramatically in processing speed, with some notorious for extended delays.

Plan conservatively by adding 50% buffer to estimated timelines for permits and licensing. Engage local professionals familiar with specific municipal procedures. Their relationships and knowledge of proper submission formats accelerate approvals.

Insufficient financial planning

Focusing solely on purchase price while ignoring transaction costs, renovation expenses, and holding costs depletes budgets prematurely. Properties requiring renovation often exceed budgets by 30-40% when investors skip detailed cost analysis.

Build comprehensive budgets including:

- All transaction taxes and fees

- Complete renovation costs with 15-20% contingency

- Holding costs during renovation and initial rental periods

- Marketing and leasing expenses

- Six months of reserves for unexpected issues

Secure financing covering your total budget, not just purchase price. Lenders may provide construction loans in tranches tied to completion milestones.

Pro Tip: Engage local experts early in your planning process. Their market knowledge, contractor networks, and bureaucratic expertise smooth processes significantly and help you avoid common investment mistakes that derail projects.

“Successful property investment in Portugal requires patience, detailed planning, and local expertise. Rushing any phase typically costs more than the time saved.”

Expected investment results and market insights

Understanding realistic return expectations helps you evaluate opportunities accurately and avoid overoptimistic projections that lead to poor decisions.

Rental yield benchmarks

Buy-to-let properties across Portugal generate average rental yields around 6.9%, though results vary significantly by location, property type, and management quality. Lisbon’s prime neighborhoods yield 3-4% due to high purchase prices, while emerging areas and secondary cities produce 7-9% yields.

Calculate gross rental yield by dividing annual rental income by total acquisition cost, including purchase price and transaction fees. Net yields account for ongoing expenses like property tax, insurance, maintenance, and property management fees, typically reducing returns by 2-3 percentage points.

Short-term vacation rentals can generate higher gross yields but involve greater management complexity, seasonal volatility, and regulatory restrictions in some municipalities. Long-term residential tenancies provide stable cash flow with lower management demands.

Price appreciation trends

Lisbon experienced annual price growth of approximately 4.8% recently, representing market maturity after years of rapid appreciation. The Setúbal region recorded price increases exceeding 22% as buyers sought more affordable alternatives to the capital with reasonable commuting access.

| Region | Annual price growth | Rental yield range | Market characteristics |

|---|---|---|---|

| Lisbon center | 4-5% | 3-4% | Mature, premium pricing, strong demand |

| Porto | 5-7% | 4-5% | Growing tech sector, improving infrastructure |

| Algarve | 3-4% | 5-7% | Tourism-driven, seasonal volatility |

| Setúbal | 18-22% | 6-8% | Emerging market, affordability appeal |

| Interior regions | 2-3% | 8-10% | Higher yields, limited liquidity |

Prime markets with established demand offer lower yields but greater liquidity and price stability. Emerging markets provide higher yield potential with increased appreciation upside but carry greater risk and longer selling timelines.

Residential versus commercial properties

Residential properties dominate foreign investment for good reasons:

- Broader tenant demand providing consistent occupancy

- Simpler management requirements for long-term rentals

- Qualification for Golden Visa residency programs

- Greater liquidity when selling

Commercial properties offer diversification benefits and potentially higher yields but require deeper market knowledge. Retail spaces face e-commerce headwinds, while office properties depend on local employment growth. Industrial and warehouse properties benefit from logistics growth but involve specialized management.

Commercial leases typically run longer terms than residential, providing stable cash flow once occupied. However, vacancy periods last longer, and tenant improvements can require significant capital.

Setting realistic expectations

Successful investors model conservative scenarios rather than best-case projections. Assume:

- Rental income 10-15% below market rates to account for vacancies and collection issues

- Annual expenses of 25-30% of gross rental income

- Renovation costs 20% above initial estimates

- Longer timelines than projected for permits, construction, and initial leasing

Review Portugal property market trends regularly to identify shifting demand patterns, emerging neighborhoods, and regulatory changes affecting returns. Markets evolve, and yesterday’s hot areas may underperform while overlooked regions gain momentum.

Pro Tip: Focus on total return combining rental income and appreciation rather than maximizing either component alone. Balanced properties in growing markets with reasonable yields and appreciation potential typically outperform over investment horizons.

Explore Springvale Estates to optimize your Portugal real estate investment

Navigating Portugal’s property market becomes significantly easier with specialized guidance from professionals who understand foreign investor needs. Springvale Estates offers comprehensive services designed specifically for American and British investors seeking residential and commercial opportunities across Portugal.

Access our network of property agencies in Portugal staffed by multilingual professionals experienced in cross-border transactions. Browse new property listings updated daily, featuring opportunities perfect for relocation, investment, and Golden Visa qualification. Use our advanced property search tools to filter by location, price range, property type, and investment criteria, finding properties matching your specific goals efficiently. Our team handles legal coordination, financing introductions, and post-purchase support, ensuring smooth transactions from initial inquiry through ownership. Let us help you avoid common pitfalls and maximize your Portuguese real estate returns with expert local knowledge and dedicated investor support.

Frequently asked questions

What documents are required to buy property in Portugal?

You need a valid passport, Portuguese Tax Identification Number, proof of funds for purchase and fees, and Portuguese bank account documentation. Your attorney will obtain property title certificates, urban planning certificates, and energy efficiency ratings as part of due diligence. Non-residents should also provide proof of address in their home country and income documentation if seeking financing.

Can foreigners get financing from Portuguese banks?

Yes, Portuguese banks offer mortgages to non-resident foreign buyers, though terms are more restrictive than resident loans. Expect maximum loan-to-value ratios of 60-70% and interest rates approximately 0.5-1% higher than resident rates. You must provide comprehensive income documentation, translated tax returns, employment verification, and proof of existing assets. Self-employed applicants face additional scrutiny requiring multiple years of consistent income demonstration.

How long does the property purchase process usually take?

Typical property acquisitions require 2.5 to 5 months from initial offer to final deed signing, though complex transactions or renovation projects extend longer. Timeline components include legal due diligence (2-3 weeks), mortgage approval (4-8 weeks), permit processing for renovations (1-6 months), and final deed preparation (2-3 weeks). Municipal bureaucracy and permit approvals cause most delays, varying significantly by location and project scope.

What taxes will I pay when buying property in Portugal?

Property transfer tax (IMT) represents the largest expense, typically 6.5-7.5% of purchase price for properties valued around €550,000. Add stamp duty at 0.8%, plus legal fees, notary costs, and registration fees, bringing total transaction costs to approximately 11% of purchase price. Annual property tax (IMI) ranges from 0.3% to 0.8% of fiscal value for ongoing ownership. Non-resident rental income faces taxation at progressive rates up to 48% or optional flat rate of 25%.

Is investing in commercial property suitable for residency purposes?

Commercial property investments can qualify for Golden Visa program details and residency pathways, though specific requirements and minimum investment thresholds vary by property type and location. Recent program changes emphasize investments in less-developed regions or specific property categories. Commercial properties offer diversification and potentially higher yields but involve greater complexity and longer management timelines than residential properties. Consult with immigration specialists to confirm current qualification criteria before purchasing with residency goals.